Unexpected Chance to Reclaim Cash: How Importing Small Businesses Can Benefit From Recent Tariff Rulings

Many small companies consider customs duties an unavoidable cost that comes with importing. Once a shipment clears U.S. borders and the tariff is paid, the money is written off and folded into pricing or margins. A recent shift in federal guidance, however, means some of those payments can now be clawed back—putting sorely needed dollars back into the pockets of small and midsized enterprises (SMEs).

Why Tariff Refunds Are Back on the Table

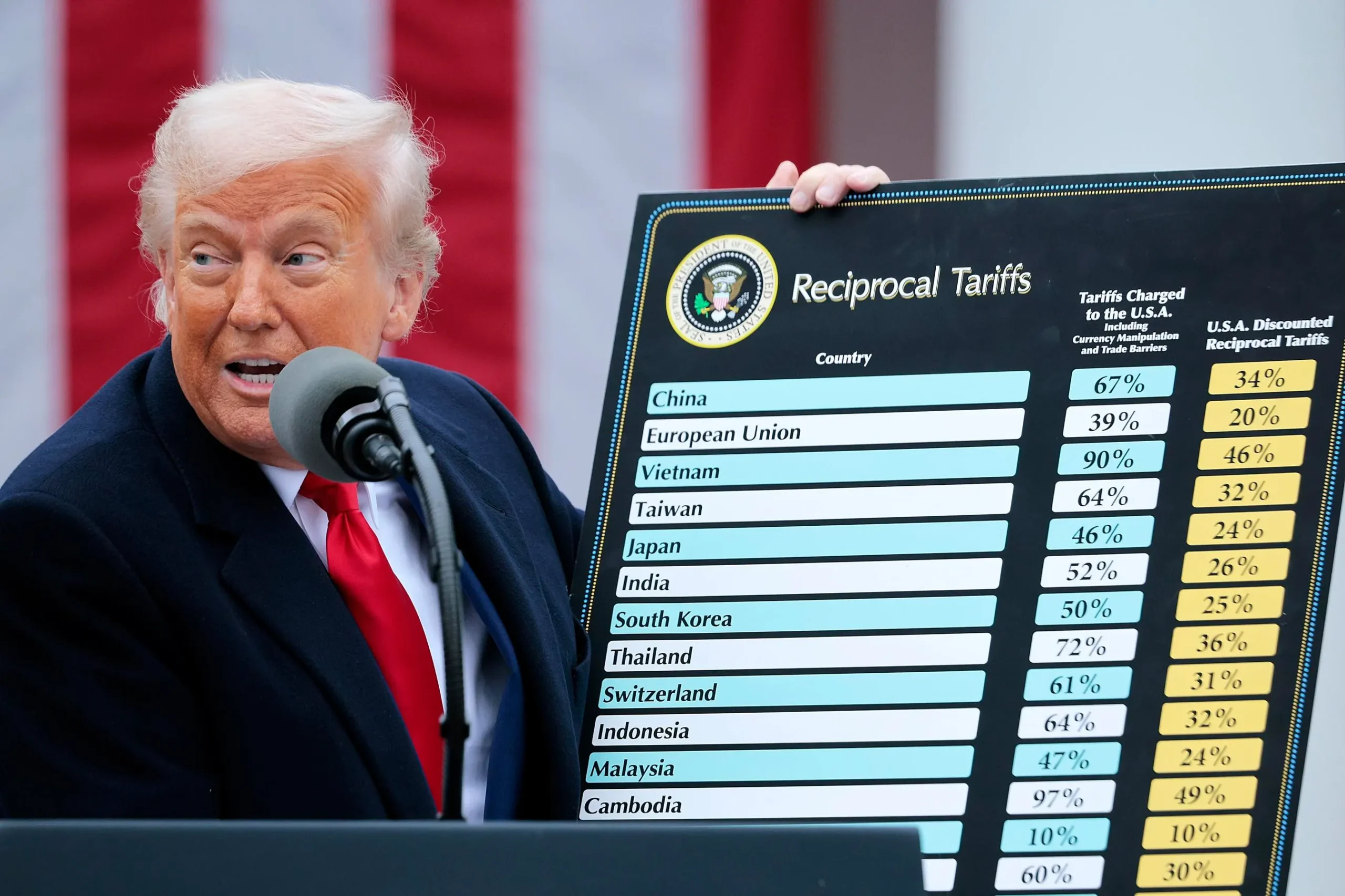

In February, the U.S. Supreme Court invalidated a set of tariffs imposed under the International Emergency Economic Powers Act (IEEPA). The court ruled that the previous administration’s sweeping tariffs on goods from a wide range of foreign partners exceeded the authority granted by that statute. Following the decision, U.S. Customs and Border Protection (CBP) issued new compliance guidance in April clarifying that importers that paid duties under the now-voided action may, in certain circumstances, request refunds.

The guidance is highly technical—typical of customs regulations—and easily overlooked by operators already juggling supply-chain issues, staffing concerns and cash-flow pressures. Yet, for eligible shipments, refunded duties can translate into tens of thousands of dollars in unanticipated liquidity.

Tariffs and the Small-Business Balance Sheet

Tariffs rarely hit all firms equally. Federal Reserve research shows that rising import duties squeeze profitability for U.S. companies, with smaller players feeling the pain first. Unlike large corporations, SMEs often lack the purchasing scale to negotiate lower prices from suppliers or the market muscle to pass surcharges on to buyers. As a result, the full cost of a tariff is absorbed in the form of thinner margins or higher borrowing needs.

Even a duty rate of a few percentage points can put pressure on working capital:

- A $50,000 shipment facing a 10% tariff locks up $5,000 in cash.

- At an annual interest rate of 8%, carrying that cost through a six-month inventory cycle adds roughly $200 in finance charges.

- Multiply that across multiple containers per year and the burden grows quickly.

That makes any avenue to recoup levies enormously valuable—particularly at a moment when credit remains tight for the smallest borrowers.

Which Duties Are Affected?

Only tariffs collected under the specific IEEPA action struck down by the Supreme Court are eligible. Other duties—antidumping, countervailing, safeguard measures, or Section 301 penalties that remain in force—are not part of the current refund opportunity.

Determining whether a past entry qualifies requires a line-by-line review of import records. Key data points include:

- Entry date and number

- Harmonized Tariff Schedule (HTS) classification

- Country of origin

- Duty type and rate applied at the time of importation

If the entry reflects an IEEPA tariff code now deemed invalid, the associated duty may be refunded—provided the claim is filed before statutory deadlines expire.

The Filing Clock Is Ticking

CBP rules give importers 180 days from the date of liquidation (the final assessment of duties) to file protests contesting or seeking refunds. For many businesses, that window may already be closing for shipments cleared early last year. Because the Supreme Court’s ruling resets the legal basis for those duties, filing deadlines can be complicated. Trade attorneys advise treating the date of CBP’s April guidance as the safest reference point, but every case should be reviewed individually.

Missing the deadline generally means forfeiting the refund. With no automatic notification system in place, importers must act on their own initiative.

Five Practical Steps to Secure a Refund

- Pull import data. Obtain entry summaries (CBP Form 7501) for the period when IEEPA tariffs were charged.

- Flag potential entries. Cross-check duty codes against the list affected by the Supreme Court decision.

- Calculate refund value. Sum the duties paid on eligible entries to ensure the amount justifies the filing effort.

- Prepare documentation. CBP typically requires a formal protest (Form 19) or Post-Summary Correction, plus supporting invoices and proof of payment.

- File before the deadline. Work with a licensed customs broker or trade attorney to meet procedural requirements and respond promptly to any CBP requests for additional information.

Common Pitfalls for Small Importers

Large multinational corporations employ in-house customs compliance teams that track regulatory developments daily. In contrast, smaller firms often outsource logistics to forwarders, leaving them with little visibility into the finer details of duty classification. The most frequent mistakes include:

- Assuming brokers automatically process refunds—most do not unless expressly instructed.

- Mistaking other trade remedies (e.g., Section 301) for IEEPA duties.

- Failing to retain complete import documentation, making it impossible to substantiate claims.

- Waiting until the final weeks to engage an advisor, only to learn that key records or signatures are missing.

Broader Policy Questions

The refund episode underscores a recurring theme in U.S. trade policy: when relief mechanisms rely on complex paperwork and tight deadlines, the benefits skew toward companies with compliance infrastructure. Policymakers often tout exemptions or rebates as evidence that small businesses are protected, but the on-the-ground reality can be quite different.

Enhancing transparency—through simple, plain-language alerts to all importers of record—and extending filing windows could make future remedies more equitable. Until then, proactive SMEs will need to stay vigilant and, where possible, join industry associations that provide early warnings about legal shifts.

Imagem: Internet

What a Successful Refund Can Do

For an importer turning $5 million in annual revenue, a $75,000 duty refund might fund:

- An additional production run ahead of a busy season

- Three months of payroll for a small team

- Interest payments on a line of credit, improving the firm’s credit score

- Investment in e-commerce upgrades or digital marketing

These tangible benefits illustrate why staying current on customs developments is more than a back-office exercise; it is an operational necessity.

Next Moves for Business Owners

Entrepreneurs who import—even sporadically—should schedule time this week to:

- Contact their customs broker for a duty profile report.

- Confirm whether IEEPA-related tariffs were applied in the past two years.

- Assess the potential dollar value of a claim.

- Engage a trade professional if the amount justifies the cost of representation.

Acting quickly maximizes the chance of recovery, while delay all but guarantees the opportunity will slip away.

Looking Ahead

Tariff policies can change overnight, sometimes by court order, sometimes by executive action. Each alteration carries costs and opportunities. For small businesses operating on thin margins, the difference between seizing and missing a fleeting refund can mean the difference between growth and contraction.

The bottom line: customs duties are not always a sunk cost. When laws shift, so too can your company’s ledger. Awareness, documentation and swift action are now the keys to turning yesterday’s tariffs into tomorrow’s cash flow.

FAQ

Q1: Which specific tariffs are eligible for refunds?

A1: Only duties collected under the IEEPA tariffs that the Supreme Court struck down in February are eligible. Other tariff programs remain in place and are not subject to the current refund process.

Q2: How much time do I have to file for a refund?

A2: Generally, you have 180 days from the date CBP liquidated the entry. Because individual timelines vary, consult a trade professional as soon as possible.

Q3: Can my customs broker automatically file the claim for me?

A3: Brokers can assist, but they typically act only when directed by the importer. Assume that no action will occur until you provide explicit instructions.

Q4: What documents are required?

A4: At minimum, you will need entry summaries, commercial invoices, proof of duty payment and a completed CBP protest or Post-Summary Correction form.

Q5: Is the refund taxable income?

A5: Refunds generally reduce the cost of goods sold rather than count as income, but tax treatment can vary. Consult a certified public accountant for guidance specific to your situation.